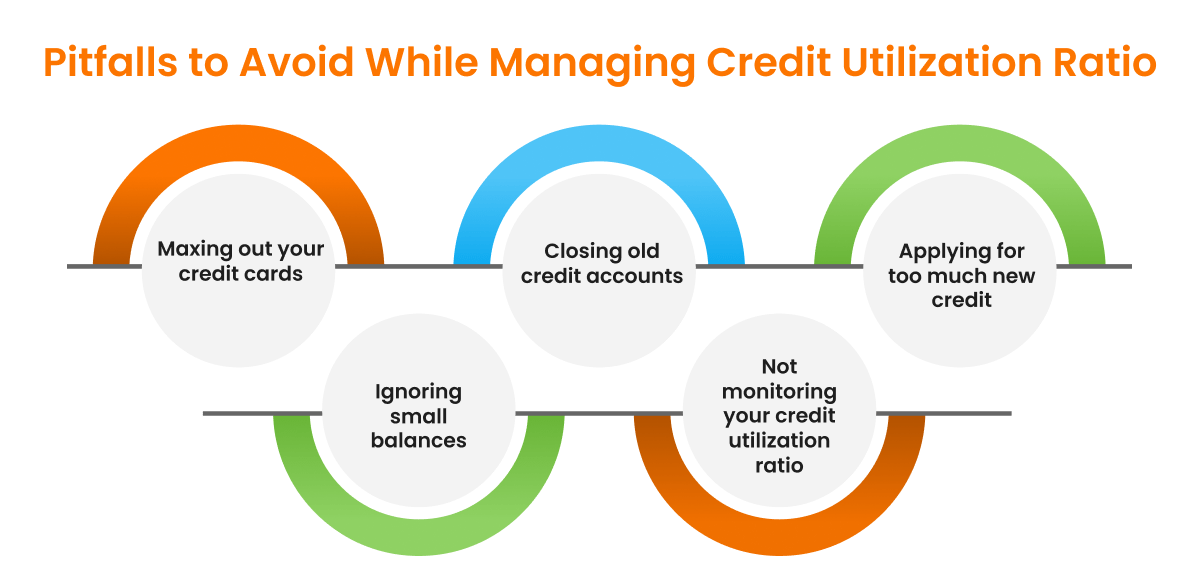

Understanding and managing your credit utilization ratio is crucial for maintaining a healthy credit score and accessing favorable financial opportunities. This ratio, a significant factor in credit scoring, represents the amount of credit you’re using compared to your total available credit. Optimizing your credit utilization ratio involves strategic planning and consistent effort. This article will delve into how to calculate this important financial metric and provide actionable strategies to lower it effectively, ultimately empowering you to take control of your financial well-being.

The credit utilization ratio (CUR) is calculated by dividing the total amount of your outstanding credit balances by your total available credit limit. For example, if you have a credit card with a $10,000 limit and a balance of $3,000, your CUR is 30%. Credit scoring models, such as FICO and VantageScore, consider CUR a key indicator of creditworthiness. A lower CUR generally suggests responsible credit management, while a higher CUR might indicate a higher risk of default.

Why is Credit Utilization Ratio Important?

- Impact on Credit Score: A lower CUR can significantly improve your credit score, making you a more attractive borrower to lenders.

- Access to Better Interest Rates: A good credit score, influenced by a healthy CUR, can help you qualify for lower interest rates on loans and credit cards.

- Increased Credit Limits: Maintaining a low CUR can increase your chances of being approved for higher credit limits;

The formula for calculating your credit utilization ratio is straightforward:

Credit Utilization Ratio = (Total Credit Used / Total Available Credit) x 100

To determine your CUR, gather the following information:

- The outstanding balance on each of your credit cards and lines of credit.

- The credit limit for each of your credit cards and lines of credit.

Add up all your outstanding balances to get your “Total Credit Used.” Then, add up all your credit limits to get your “Total Available Credit.” Finally, plug these numbers into the formula.

Example:

You have two credit cards:

- Card 1: $2,000 balance, $5,000 credit limit

- Card 2: $1,000 balance, $10,000 credit limit

Total Credit Used: $2,000 + $1,000 = $3,000

Total Available Credit: $5,000 + $10,000 = $15,000

Credit Utilization Ratio: ($3,000 / $15,000) x 100 = 20%

Lowering your credit utilization ratio requires a proactive approach. Here are several effective strategies you can implement:

- Pay Down Balances: The most direct way to lower your CUR is to pay down your outstanding balances. Aim to pay more than the minimum payment each month.

- Increase Credit Limits: Request a credit limit increase from your credit card issuers. A higher credit limit will lower your CUR, even if your spending remains the same. However, be responsible and avoid the temptation to overspend.

- Open a New Credit Card: Applying for a new credit card can increase your overall available credit, thus lowering your CUR. Be mindful of the impact on your credit score from opening a new account.

- Utilize Balance Transfers: Consider transferring high balances from cards with high utilization to cards with lower utilization. This can provide temporary relief and help lower your overall CUR.

- Time Your Payments: Credit card companies typically report your balance to credit bureaus once a month. Make a payment a few days before the reporting date to lower the balance that’s reported.

| Strategy | Pros | Cons |

|---|---|---|

| Balance Transfers | Can lower overall interest paid, improves CUR quickly. | May involve transfer fees, requires approval, potential for increased spending. |

| Paying Down Balances | Reduces debt, improves financial health, no fees. | Requires discipline and budgeting, may take longer to see results. |

Understanding and managing your credit utilization ratio is crucial for maintaining a healthy credit score and accessing favorable financial opportunities. This ratio, a significant factor in credit scoring, represents the amount of credit you’re using compared to your total available credit. Optimizing your credit utilization ratio involves strategic planning and consistent effort. This article will delve into how to calculate this important financial metric and provide actionable strategies to lower it effectively, ultimately empowering you to take control of your financial well-being.

Understanding Credit Utilization Ratio

The credit utilization ratio (CUR) is calculated by dividing the total amount of your outstanding credit balances by your total available credit limit. For example, if you have a credit card with a $10,000 limit and a balance of $3,000, your CUR is 30%. Credit scoring models, such as FICO and VantageScore, consider CUR a key indicator of creditworthiness. A lower CUR generally suggests responsible credit management, while a higher CUR might indicate a higher risk of default.

Why is Credit Utilization Ratio Important?

- Impact on Credit Score: A lower CUR can significantly improve your credit score, making you a more attractive borrower to lenders.

- Access to Better Interest Rates: A good credit score, influenced by a healthy CUR, can help you qualify for lower interest rates on loans and credit cards.

- Increased Credit Limits: Maintaining a low CUR can increase your chances of being approved for higher credit limits.

Calculating Your Credit Utilization Ratio

The formula for calculating your credit utilization ratio is straightforward:

Credit Utilization Ratio = (Total Credit Used / Total Available Credit) x 100

To determine your CUR, gather the following information:

- The outstanding balance on each of your credit cards and lines of credit.

- The credit limit for each of your credit cards and lines of credit.

Add up all your outstanding balances to get your “Total Credit Used.” Then, add up all your credit limits to get your “Total Available Credit.” Finally, plug these numbers into the formula.

Example:

You have two credit cards:

- Card 1: $2,000 balance, $5,000 credit limit

- Card 2: $1,000 balance, $10,000 credit limit

Total Credit Used: $2,000 + $1,000 = $3,000

Total Available Credit: $5,000 + $10,000 = $15,000

Credit Utilization Ratio: ($3,000 / $15,000) x 100 = 20%

Strategies to Lower Your Credit Utilization Ratio

Lowering your credit utilization ratio requires a proactive approach. Here are several effective strategies you can implement:

- Pay Down Balances: The most direct way to lower your CUR is to pay down your outstanding balances. Aim to pay more than the minimum payment each month.

- Increase Credit Limits: Request a credit limit increase from your credit card issuers. A higher credit limit will lower your CUR, even if your spending remains the same. However, be responsible and avoid the temptation to overspend.

- Open a New Credit Card: Applying for a new credit card can increase your overall available credit, thus lowering your CUR. Be mindful of the impact on your credit score from opening a new account.

- Utilize Balance Transfers: Consider transferring high balances from cards with high utilization to cards with lower utilization. This can provide temporary relief and help lower your overall CUR.

- Time Your Payments: Credit card companies typically report your balance to credit bureaus once a month. Make a payment a few days before the reporting date to lower the balance that’s reported.

Comparing Strategies: Balance Transfers vs. Paying Down Balances

| Strategy | Pros | Cons |

|---|---|---|

| Balance Transfers | Can lower overall interest paid, improves CUR quickly. | May involve transfer fees, requires approval, potential for increased spending. |

| Paying Down Balances | Reduces debt, improves financial health, no fees. | Requires discipline and budgeting, may take longer to see results. |

Let me tell you about my own journey with credit utilization. I remember a few years back, my credit score took a nosedive. I couldn’t figure out why until I finally dug into the details and discovered my credit utilization was sky-high – hovering around 70%! I, Alex, a name I’ve decided to use for privacy, had been mindlessly swiping my credit card for everyday expenses without really tracking how much I was spending relative to my limits.

My Personal Strategies and Results

The first thing I did was calculate my CUR for each card and overall. It was a sobering experience. Armed with that knowledge, I started implementing the strategies I’ve outlined above. I decided to focus on two main approaches: aggressively paying down balances and requesting credit limit increases. Balance transfers felt risky for me, as I was worried I would spend even more.

Paying Down Balances: My Approach

I created a budget and committed to putting any extra money towards my credit card with the highest interest rate. It was tough, but I cut back on eating out and other non-essential spending. I even started selling some old items online. Slowly but surely, I saw my balances decrease. This was really effective for me because I could see tangible progress. I felt more in control.

Requesting Credit Limit Increases: A Surprising Outcome

I was initially hesitant to ask for credit limit increases, fearing it would negatively impact my credit score. However, after doing some research, I learned that it could actually help, especially if I didn’t increase my spending. I contacted my credit card issuers and requested increases on two of my cards. To my surprise, both were approved! This immediately lowered my overall CUR, even before I made significant progress on paying down my balances. It felt like a real win.

The Impact and Lessons Learned

Within a few months of consistently implementing these strategies, I saw a significant improvement in my credit score. Not only that, but I also felt more financially responsible and in control of my spending habits. It was a wake-up call that taught me the importance of actively managing my credit and understanding the impact of something as seemingly simple as the credit utilization ratio. I now track my CUR regularly and make sure to keep it below 30%, ideally closer to 10%. From my experience, I highly recommend you take the time to analyze your spending habits and make a conscious effort to improve your CUR. You’ll be surprised at the positive impact it can have on your financial life.