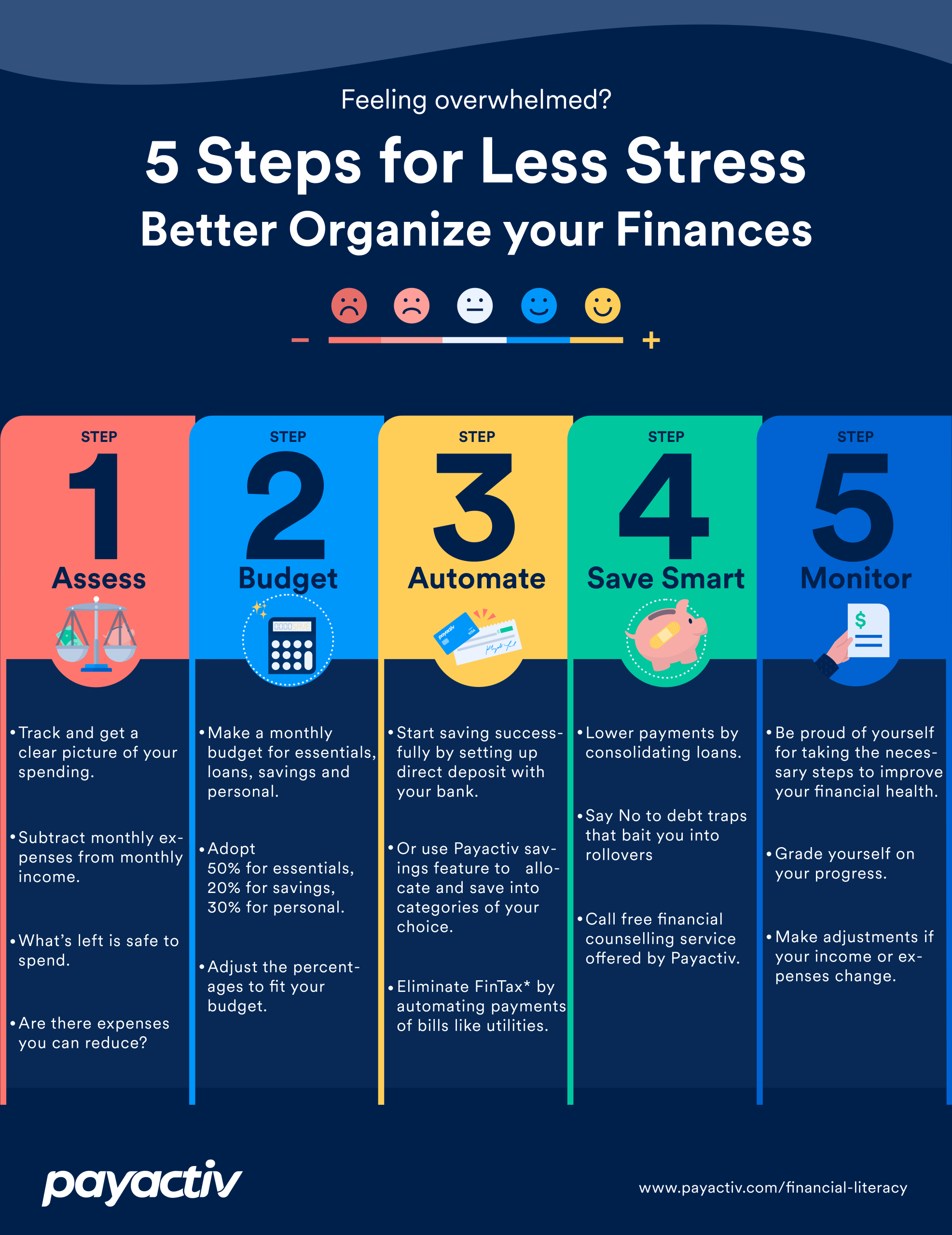

Taking control of your financial life can seem daunting, but understanding where your money goes is the first crucial step towards building a secure future. Many people avoid delving into their finances, fearing what they might find, but ignoring the situation only exacerbates potential problems. Mastering the art of calculating your finances allows you to make informed decisions, set realistic goals, and ultimately achieve financial freedom. Therefore, let’s explore five effective methods to calculate your finances and gain a clear picture of your current financial standing.

1. Creating a Detailed Budget

A budget is a fundamental tool for financial management. It’s a roadmap that outlines your income and expenses, providing insights into where your money is being allocated. A well-structured budget allows you to identify areas where you can cut back and save more.

How to Build a Budget:

- Track Your Income: List all sources of income, including salary, investments, and side hustles.

- List Your Expenses: Categorize your expenses into fixed (rent, mortgage, insurance) and variable (groceries, entertainment) costs.

- Use Budgeting Tools: Utilize budgeting apps, spreadsheets, or even a simple notebook to track your spending.

- Regularly Review and Adjust: Budgets are not static; adjust them as your income or expenses change.

2. Calculating Your Net Worth

Net worth is a snapshot of your financial health at a specific point in time. It’s calculated by subtracting your liabilities (debts) from your assets (what you own). A positive net worth indicates that you own more than you owe, while a negative net worth suggests the opposite.

Assets vs. Liabilities:

- Assets: Include cash, investments (stocks, bonds, real estate), savings accounts, and personal property (cars, jewelry).

- Liabilities: Encompass debts like credit card balances, loans (student, auto, mortgage), and outstanding bills.

3. Tracking Your Cash Flow

Cash flow refers to the movement of money in and out of your accounts. Understanding your cash flow helps you identify spending patterns and areas for improvement. Positive cash flow means you’re earning more than you’re spending, allowing you to save and invest. Negative cash flow indicates that you’re spending more than you earn, potentially leading to debt accumulation.

4. Analyzing Your Debt-to-Income Ratio (DTI)

The debt-to-income ratio (DTI) is a percentage that compares your monthly debt payments to your gross monthly income. Lenders often use DTI to assess your ability to repay loans. A lower DTI generally indicates a healthier financial situation.

DTI Calculation:

Total Monthly Debt Payments / Gross Monthly Income = DTI Ratio

For example, if your total monthly debt payments are $1,500 and your gross monthly income is $5,000, your DTI is 30% ($1,500 / $5,000 = 0.30).

5. Using Financial Calculators and Tools

Numerous online financial calculators and tools can assist you in various calculations, such as mortgage amortization, retirement planning, and investment returns. These tools can provide valuable insights and help you make informed financial decisions. They automate complex calculations and present the results in an easily understandable format.

Beyond these core calculations, it’s important to remember that financial well-being is a holistic concept. It’s not solely about crunching numbers; it’s also about developing healthy financial habits, such as saving regularly, avoiding unnecessary debt, and investing wisely. These habits, combined with a clear understanding of your financial situation, create a powerful synergy that propels you towards long-term financial security.

The Importance of Regular Review

Once you’ve established these methods for calculating your finances, the next crucial step is to implement a regular review process. Financial landscapes are constantly shifting due to changes in income, expenses, market conditions, and personal circumstances. What worked effectively six months ago might not be optimal today. Therefore, a consistent review schedule is essential.

Benefits of Regular Review:

- Early Identification of Problems: Regular reviews allow you to spot potential financial issues early on, such as overspending, increasing debt, or declining investment performance. Addressing these issues promptly can prevent them from escalating into larger problems.

- Opportunity for Optimization: As your financial situation evolves, you may discover opportunities to optimize your strategies. This could involve refinancing debt at a lower interest rate, adjusting your investment portfolio, or increasing your savings rate.

- Reinforcement of Positive Habits: Regularly reviewing your finances reinforces positive habits and keeps you motivated to stay on track towards your financial goals; Seeing your progress and the positive impact of your efforts can be incredibly rewarding.

- Adaptation to Life Changes: Life events such as marriage, the birth of a child, a job change, or retirement can significantly impact your finances. Regular reviews ensure that your financial plan is aligned with your current life circumstances.

Tools and Resources for Financial Calculation and Review

Fortunately, a wide array of tools and resources are available to simplify financial calculations and facilitate regular reviews. These tools range from simple spreadsheets to sophisticated software programs and online platforms. Choosing the right tools depends on your individual needs, preferences, and technical expertise.

Types of Tools and Resources:

- Budgeting Apps: These apps automate expense tracking, categorize transactions, and provide insights into your spending habits. Many budgeting apps also offer features such as goal setting, debt tracking, and investment monitoring.

- Financial Planning Software: Comprehensive financial planning software can help you create detailed financial plans, model different scenarios, and track your progress towards your goals. These programs often include features for retirement planning, investment analysis, and estate planning.

- Spreadsheets: Spreadsheets are a versatile tool for creating budgets, tracking expenses, calculating net worth, and analyzing cash flow. They offer a high degree of customization and allow you to tailor your calculations to your specific needs.

- Online Calculators: Numerous online calculators are available for specific financial calculations, such as mortgage amortization, retirement savings, and investment returns. These calculators can provide quick and accurate estimates for various scenarios.

- Financial Advisors: For those who prefer personalized guidance, working with a qualified financial advisor can be invaluable. A financial advisor can help you develop a comprehensive financial plan, make informed investment decisions, and navigate complex financial situations.

Ultimately, taking control of your financial future requires a proactive and informed approach. By consistently calculating your finances, regularly reviewing your progress, and leveraging the available tools and resources, you can build a solid foundation for long-term financial security and achieve your financial goals.